In today’s evolving mortgage landscape, nontraditional credit guidelines are more than just a workaround, they’re a powerful tool for expanding access to homeownership. At Enact, we recognize that not every borrower fits the mold of traditional credit profiles. That’s why understanding and applying nontraditional credit guidelines can be a game-changer in final underwriting decisions.

Our own Amy Hopkins, Regional Underwriter, shares her expertise on nontraditional credit guidelines, how Enact MI handles this credit path, and industry guidance from the GSEs.

Why nontraditional credit matters

Borrowers may need to pursue nontraditional credit paths for a variety of reasons: they might be recent graduates, immigrants, or individuals who prefer to operate on a cash basis. These borrowers often lack the conventional tradelines that appear on a Residential Mortgage Credit Report (RMCR), yet they demonstrate financial responsibility in other meaningful ways.

Nontraditional credit allows lenders to consider a broader spectrum of payment history—rent, utilities, insurance, and more—to build a fuller picture of a borrower’s creditworthiness. This shift moves beyond rigid metrics and opens doors for diverse borrowers who might otherwise be excluded from traditional financing options.

Traditional vs. nontraditional credit

Traditional credit is defined by the presence of credit scores and verified tradelines on an RMCR. These tradelines must meet specific criteria, such as months reviewed and satisfactory payment history. For loans underwritten with Enact MI, we defer to Fannie Mae and Freddie Mac guidelines to determine whether a borrower meets traditional credit standards.

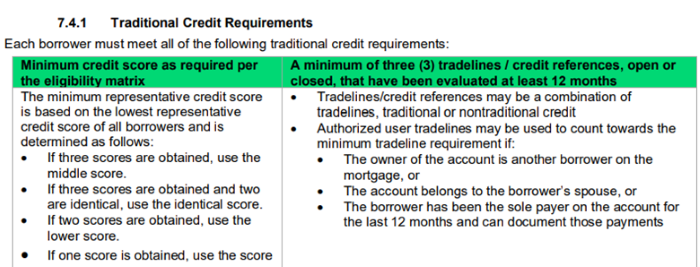

Enact MI underwriting guidelines are very specific on what we require for a borrower using traditional credit guidelines. See Section 7.4.1 below for outlined traditional credit requirements.

However, if a borrower doesn’t meet these standards, or if the loan is manually underwritten, nontraditional credit becomes a viable alternative. If a lender is using an Automated Underwriting System (AUS), it’s essential to review the AUS findings, which will clearly indicate whether additional documentation is needed to support the borrower’s credit profile.

Enact's approach to nontraditional credit

When traditional credit isn’t available on the RMCR, Enact MI’s guidelines (see Section 4.9) outline acceptable sources of nontraditional credit. These include:

- Rental housing payments. This includes payments made to a landlord or management company. Also included are payments made on a privately-held mortgage loan that is not reported to the credit bureaus, contract for deed payments and other similar arrangements, provided the payments are related to the Borrower’s housing.

- Utilities, such as electricity, gas, water, telephone service, television, and internet service providers. If utilities are included in the rental housing payment, they cannot be considered a separate source of nontraditional credit. Utilities can be considered a source of nontraditional credit only if the payment history can be separately documented.

- Medical insurance coverage (excluding payroll deductions)

- Automobile insurance payments

- Cell phone payments

- Life insurance policies (excluding payroll deductions)

- Payments for household or renter’s insurance

- Payments to local stores, such as department stores, furniture stores, appliance stores

- Rental payments for durable goods, such as automobiles

- Payment of medical bills

- Payment of school tuition

- Payments for childcare

- A loan obtained from an individual, provided the repayment terms can be documented in a written agreement

- Checking account, savings account, voluntary payments made to a payroll savings plan or contributions to a stock purchase plan, provided the records reflect an increasing balance as a result of periodic deposits over at least the most recent 12 months. Contributions must have been made no less than quarterly.

- Wire remittance statements demonstrating a consistent amount of funds remitted over the most recent 12-month period.

These sources help paint a more complete financial picture, especially when traditional credit data is limited or unavailable.

Agency guidance and investor considerations

Enact's nontraditional credit guidelines are for loans not meeting GSE AUS nontraditional credit loan requirements. Therefore, Enact's guidelines as referenced in Section 4.9 may differ in some respects than what the GSEs will allow. It’s important to remember that if your loan receives a Desktop Underwriter® (DU®) approve/eligible or Loan Product Advisor® (LPA®)accept/eligible recommendation, you should follow the AUS findings. For loans sold to investors other than Fannie Mae or Freddie Mac, confirm their specific requirements regarding nontraditional credit. Access Fannie Mae or Freddie Mac guidelines anytime to help you navigate this nontraditional credit path.

More ways we at Enact can help

We understand that nontraditional credit guidelines empower lenders to make informed decisions to help reflect the realities of today’s borrowers. By embracing these flexible standards, we help more people achieve the dream of homeownership—one thoughtful loan at a time. That’s why when you’re working with borrowers who may not have traditional credit history, your Enact MI team has you covered. Our Regional Underwriting Team is available to assist you Monday-Friday 8am to 8pm ET at 800-444-5664 option 2. We look forward to working with you!

Be sure to make the most of your MI experience, too. Explore our many underwriting resources and underwriting tips, as well as our comprehensive suite of training resources to help boost your industry experience.

Source: Amy Hopkins is a Regional Underwriter for Enact.

The statements in this article are solely the opinions of Amy Hopkins and do not necessarily reflect the views of Enact or its management.

Never miss a post by subscribing to Enact MI’s Discover360℠ Blog! We’ll send you our most up-to-date topics right into your inbox.