[Video] 5 Tips to Working with Self-Employed Borrowers

With volume at historically high levels, you can’t afford to lose time on originating loans. That’s why when tricky loan applications come your way, like ones from self-employed borrowers, you want to know exactly what to do and what kind of information you need to save time.

In this post we’ll discuss some of our top tips to know before you begin working with self-employed borrowers.

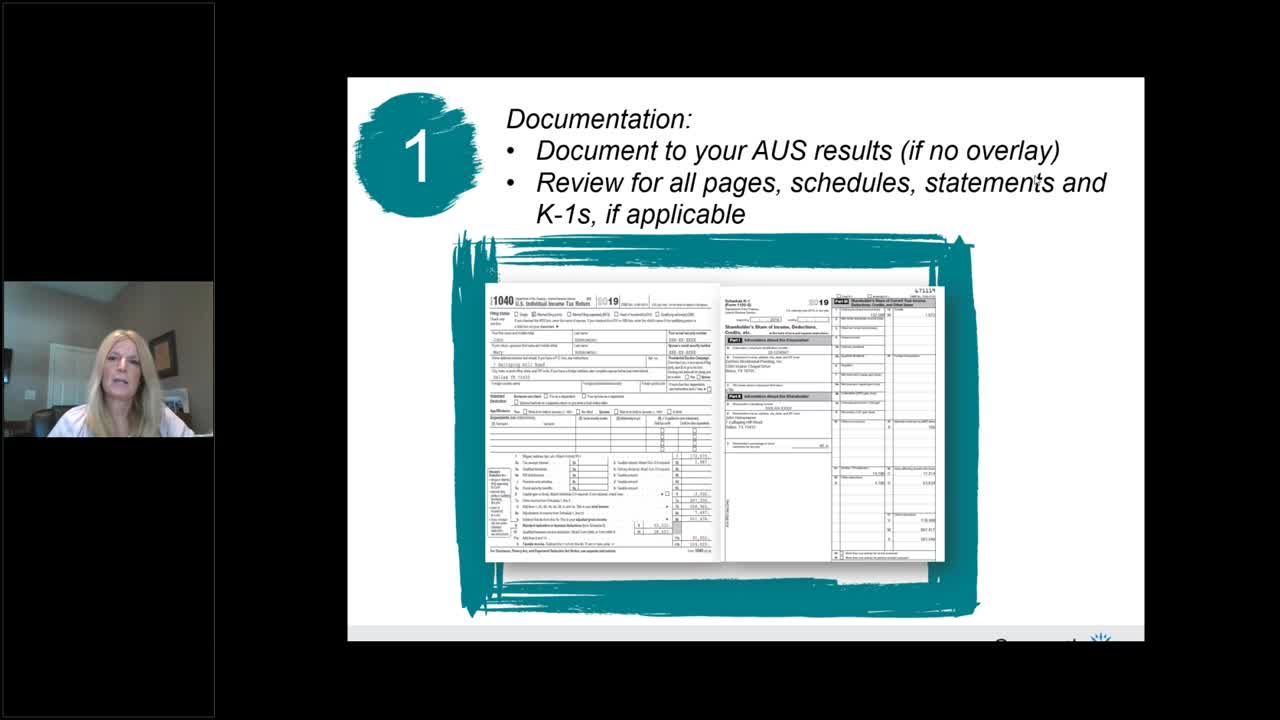

Tip #1: Check for Proper Documentation

Files for self-employed borrowers that go to underwriting without proper documentation are one of the biggest time sucks we see.

If you’re using an AUS, your feedback certificates will show you which documents you need, just be sure to check the certificate. If there are overlays, you should check for the documentation required for your investor.

While you may think you have all the documentation for self-employed borrowers committed to memory, you should still check the feedback certificate and investor overlay documentation to ensure you have everything to save yourself time down the line.

One other document to keep in mind is the tax return. Know what’s required for the tax return and how to tell when certain schedules are required based on recent tax years. The K-1 schedule which shows ownership in a partnership or Chapter S business is often missing from self-employed borrower files.

Tip #2: Take Training Courses

In these busy times, you may think you don’t have 30-60 minutes to take a training course. But consider if you committed that amount of time each month to being informed on changes or brushing up on self-employed file skills, how quickly you could earn that time back.

Why? Because you won’t have to go back and forth on the file to re-calculate income or chase down additional documents.

Enact offers self-employed training for free with a variety of live and on-demand courses for you to take whenever it suits your schedule.

Tip #3: Have a Written Analysis in Your File

With self-employed borrowers, you’ll want to have a written explanation of how you calculated income the way you did. Fannie Mae and Freddie Mac actually require you to have an income analysis in your file, but it’s a best practice with any investor.

Something else you You’can include in the file for particularly tricky situations is a sheet of notes or comments to the underwriter. Having a cover letter or notes can help give context to your calculation based on conversations you’ve had with the applicant. You can also keep notes in your conversation log or the notes section of your LOS so those comments follow the file all the way to close.

Tip #4: Tax Filing Date Was Extended to July 15, 2020

While the tax deadline was extended by 3 months this year, keep in mind it’s possible even with this extension that individuals still could have requested an extension to file their taxes. That means you may still need tax returns from 2017 and 2018 rather than 2018 and 2019.

Something else to remember is if you have in-progress files where the applicant submitted their taxes right at the deadline, you may need to request a copy of the return and re-calculate the income.

Tip #5: Be Aware of COVID-19 Updates from the GSEs

As the pandemic and its impacts on the economy continue to evolve, the GSEs are continuously updating their guidelines and requirements. Some notable requirements include:

- You must provide a profit and loss statement in your file;

- The business’ operations and location must be reviewed;

- Complete a trends analysis on the calculation of income; and

- The business must be open and operating 10 days prior to the Note date

The points discussed above can be boiled down to two main principles: check your documents and remain aware of changes going on for self-employed borrower documentation and overarching guideline and requirement changes.

By working through your mental checklist of “did I check for this document” and “have I made sure there aren’t new pandemic updates,” you can save yourself considerable time down the road when your underwriter comes back to tell you that you have to chase down a document or re-calculate the income.

Keep these tips handy before you begin working with a self-employed borrower and check out our post on the power of checklists which may give you inspiration to create your own self-employed borrower checklist.

Leave a Reply

Want to join the discussion?Feel free to contribute!