Help for FTHBs: The Do’s and Don’ts of the Mortgage Process

[This 4-part series features a deep dive into each of Enact’s FTHB topics. We have other topics in a previous series that details the benefits of MI, terms and people your borrowers should know, and affordability and budget worksheets. Be sure to check out the Help for FTHBs Hub for these flier resources!]

The mortgage loan process might be your everyday bread and butter, but this may be the first time your borrowers have ever had to work with or understand the mortgage process. Your FTHBs’ mortgage loan application process can be easier with a little bit of advance planning. That’s where you come in! Their post-application process can also be much smoother when they keep in mind what activities might slow down their closing.

What do your FTHBs come to you with questions about the most? If it’s anything related to the mortgage process, we might just have what you need. FTHBs should be aware of the following Do’s and Don’ts when they decide they want to start the homebuying process, as there are many details and moving parts to get a mortgage loan.

Download the “Mortgage Process: Do’s and Don’ts” Sheet to distribute to your potential FTHBs.

Do’s when your FTHBs plan to apply:

Refer to the list below for a few of the key items/tips you’ll want to explain to your FTHBs to keep them on track during the mortgage loan application process. Even if you’re already reminding them throughout the mortgage process of these, giving them a list or handout will help them keep track of all of these moving pieces.

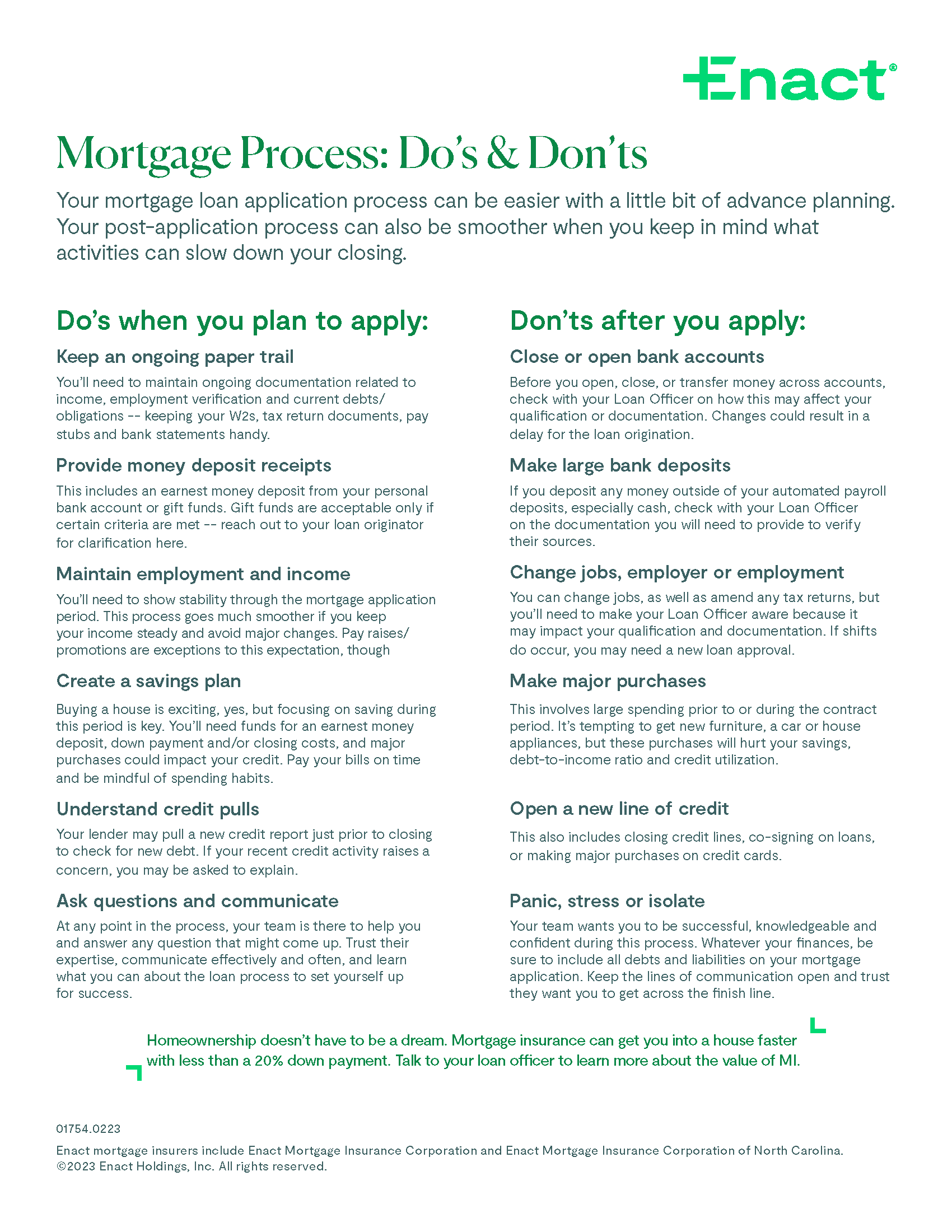

Keep an ongoing paper trail

FTHBs should maintain ongoing documentation related to income, employment verification and current debts/obligations — keeping their W2s, tax return documents, pay stubs and bank statements handy.

Provide money deposit receipts

This includes an earnest money deposit from their personal bank account or gift funds. Gift funds are acceptable only if certain criteria are met – be sure to clarify this for your individual FTHB’s situation.

Maintain employment and income

Your FTHBs need to show stability throughout the mortgage application period. This process goes much smoother if your borrowers keep their income steady and avoid major changes. Pay raises/promotions are exceptions to this expectation, though.

Create a savings plan

Buying a house is an exciting time for any homebuyer, yes, but focusing on saving during this period is key for them. They’ll need funds for an earnest money deposit, down payment and/or closing costs, and major purchases could impact their credit.

Understand credit pulls

They’ll need to be mindful that you may pull a new credit report just prior to closing to check for new debt. If their recent credit activity raises a concern, you’ll need to ask them to explain.

Ask questions and communicate

At any point in the process, your team should be there to help your FTHBs and answer any questions that they might have – establishing that relationship and being open with them goes a long way!

Don’ts after your FTHBs apply:

Check out the list below for a few of the key items/tips you’ll want to explain to your FTHBs to keep them on track after they’ve applied for a mortgage loan. Continue to work with your borrowers and give them our handout to help them keep track of all the moving pieces during this process.

Close or open bank accounts

Before your FTHBs open, close, or transfer money across accounts, they should check with you on how this may affect their qualification or documentation. Remind them that changes could result in a delay for the loan origination.

Make large bank deposits

If they deposit any money outside of their automated payroll deposits, especially cash, they should check with you on the documentation they’ll need to provide to verify their sources.

Change jobs, employer or employment

They can change jobs, as well as amend any tax returns, but they’ll need to make you aware because it may impact their qualification and documentation. If shifts do occur, they may need a new loan approval.

Make major purchases

This involves large spending prior to or during the contract period. It’s tempting for your FTHBs to want to get new furniture, a car or house appliances, but these purchases may hurt their savings, debt-to-income ratio and credit utilization.

Open a new line of credit

This also includes closing credit lines, co-signing on loans, or making major purchases on credit cards.

Panic, stress or isolate

You want your borrowers to be successful, knowledgeable, and confident during this process. Whatever their finances, help them stay in the loop and remind them to be sure to include all debts and liabilities on their mortgage application. Keep the lines of communication open and they’ll trust you to help them across the finish line.

Download our “Mortgage Process: Do’s and Don’ts” Sheet below – it’s a great resource to share with your borrowers and can help you supplement any of the resources you may already have. Now available in Spanish!

Want to learn more?

You can always refer to our Help for FTHBs Hub for more resources to help your first-time and other prospective borrowers. Our dedication to helping borrowers achieve the dream of homeownership doesn’t stop here — we offer training resources to help you work with your customers to your max potential.

And, if you want to learn more about ways to better aid your FTHBs or need some extra insight, you can always contact your Enact Sales Rep for more info. They’ll be happy to help you meet your business needs, answer questions, and point you in the right direction.

Never miss a post by subscribing to the Enact MI Blog! We’ll send you our most up-to-date topics right into your inbox.

Leave a Reply

Want to join the discussion?Feel free to contribute!